DMX Projects 1.5x Earnings Growth; Management Reaffirms Undemanding Valuation

DMX management reaffirms confidence in at least 1.5x YoY NPAT growth for the full year, maintaining the current P/E is below intrinsic value - notwithstanding investor concerns that post-IPO valuations are approaching fair value and creating overhang on MWG's capitalisation.

While DMX management holds that shares are offered at a discount to intrinsic value, certain institutional investors have flagged that DMX's post-IPO valuation is approaching the market capitalization of its parent, MWG, raising questions over the balance between value creation and valuation risk.

Attractive Entry Point Into a High-Growth Story

DMX delivered FY2025 NPAT of VND 6,100bn, with the IPO price implying a trailing P/E of ~14.5x. The FY2026 NPAT target of VND 7,300bn+, approved at the April AGM, compresses the forward P/E to ~12x — an undemanding multiple relative to regional retail peers.

At the IPO investor briefing held in Ho Chi Minh City on 28 May, CEO Doan Van Hieu Em expressed confidence that FY2026 earnings could grow by at least 1.5x YoY, compressing the forward P/E to approximately 10x by year-end and implying further re-rating potential from the IPO offer price.

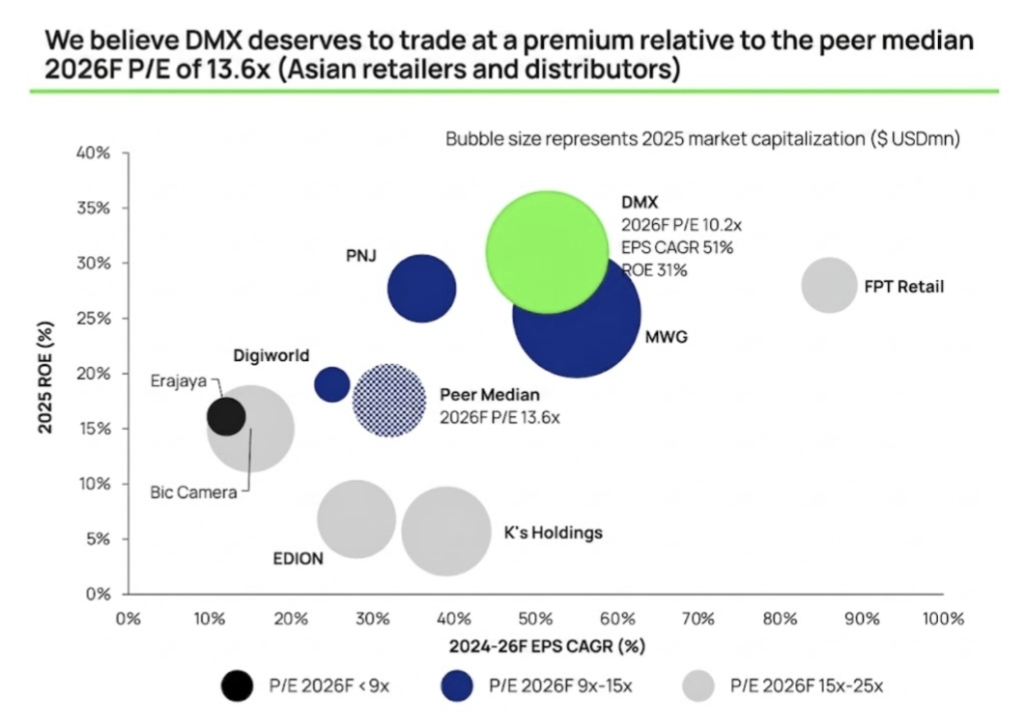

Vietcap Securities' Head of Research, Hoang Nam, cited a sector median P/E of approximately 13.6x across Asian consumer electronics retailers. At a forward P/E of around 12x, even assuming NPAT exceeds VND 7,000bn, DMX continues to trade at a discount to the peer group, with many comparable companies commanding valuation multiples of 15–25x.

Expanding Contribution Mix

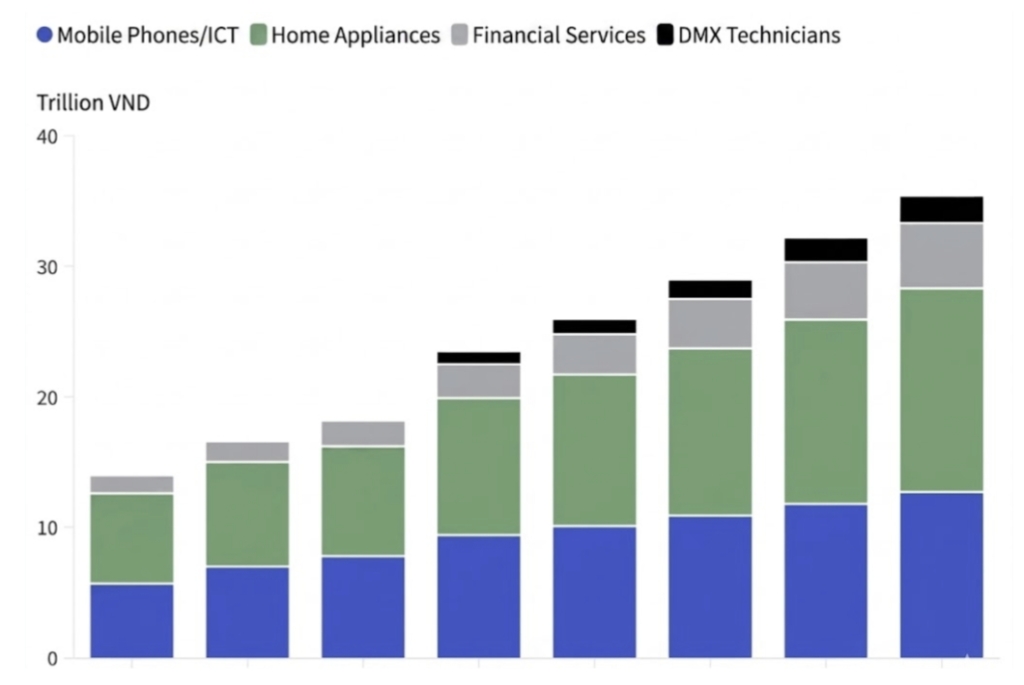

The services segment is projected to double its gross profit contribution from 10% in FY2025 to 20% by FY2030, reflecting a structural mix shift toward higher-margin revenue streams.

Vietcap's mid-May research update projects a three-year like-for-like revenue CAGR of approximately 14% and an EPS CAGR of 24% for DMX. The services segment is expected to emerge as a key earnings driver, with its gross profit contribution expanding from around 10% to 18% by FY2028, while core mobile and home appliance categories continue to deliver solid growth.

In written correspondence, Mr. Thomas Lanyi reiterated his conviction in DMX's margin expansion potential, citing improved monetisation of both physical and digital retail space as a key earnings lever. He highlighted multiple catalysts that could support sustained above-average earnings growth over the medium term, including domestic platform optimisation, scaling of the services segment, and international expansion through the Erablue chain in Indonesia.

DMX intends to distribute a cash dividend of VND 4,000 per share (equivalent to approximately 5% of the IPO offer price) shortly after listing, with payment expected in early August following its HOSE debut. The Company’s long-term dividend policy targets a minimum payout ratio of 50% of NPAT. Assuming FY2026 NPAT reaches at least VND 7,300bn, the implied cash dividend pool would amount to approximately VND 3,700bn, translating into a dividend yield of around 3–4% based on the IPO offer price.

Source: Bloomberg