DMX CEO: When the Goal Is Not Capital Flows, But a New Cycle

Holding 55% of the domestic market, where does DMX's next leg of growth come from?

A market-leading position of over 50% in Vietnamese consumer electronics retail provides DMX with a strong platform to unlock superior growth opportunities ahead. The IPO represents more than a capital event - it is the inflection point for a deliberate model transition toward a fully integrated service chain and the development of new international growth drivers.

Speaking at VNDirect Securities' "Dinsights June: DMX IPO Investment Opportunity" forum, Doan Van Hieu Em - MWG Board Member and CEO of DMX - engaged in a substantive dialogue with Nguyen Vu Long, CEO of VNDirect, and Pham Thi Bich Ngoc, Head of Consumer & etail Research.

Drawing on two decades with the company - from his early years as an accountant to his current role at the helm - Hieu Em offered a candid perspective on DMX's core growth pillars and long-term strategic vision. Addressing the market's central question, "Why now for the IPO?", he framed the listing not as a financing exercise, but as a strategic step in positioning the Company for its next phase of growth.

The "sine curve reset" strategy

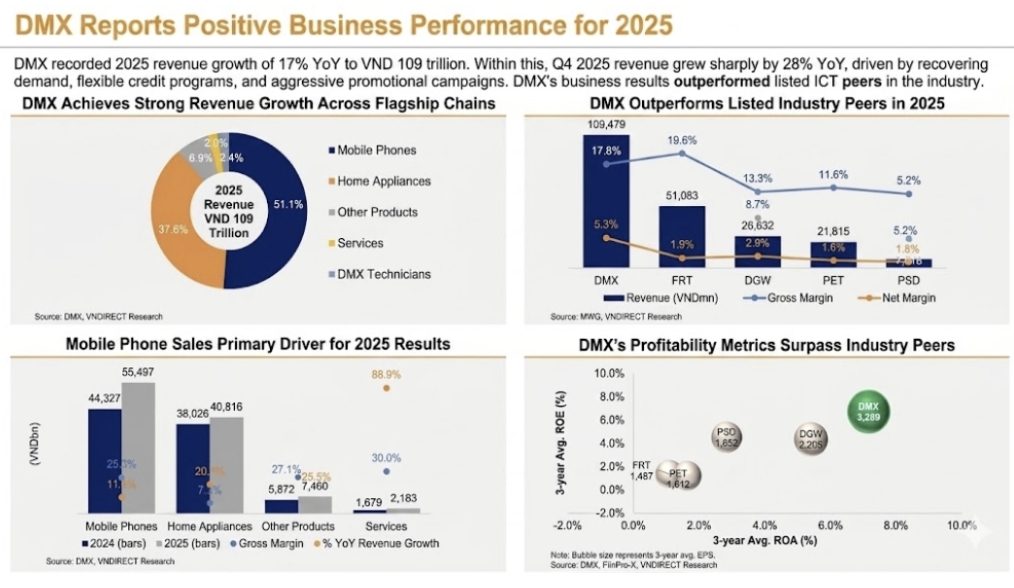

FY2025 marked a landmark year for DMX. Revenue approached USD 4bn, reinforcing the Company's dominant 55% share of Vietnam's consumer electronics retail market. Following a period of sector-wide headwinds, profitability has recovered meaningfully, with margins expanding for a second consecutive year.

Rather than consolidating gains at the cycle peak, DMX's management has elected to pursue a new growth trajectory through the IPO. CEO Doan Van Hieu Em articulated the underlying philosophy: "DMX stands at the top of a development cycle. Yet rather than seeking to extend the existing peak, we have chosen to build an entirely new cycle - with bigger challenges, and bigger goals to pursue."

This landmark IPO is not principally a capital mobilisation event - it is a strategic catalyst for the comprehensive repositioning of DMX as a business. At an offer price of VND 80,000 per share, with formal listing on HOSE targeted for August 2026, DMX is pursuing a clear strategic objective: USD 7 billion in revenue by FY2030 - representing approximately 70% growth on the current base - while generating superior equity value for shareholders who participate in this journey.

Two decades building the tree - now the deliberate work of pruning for growth

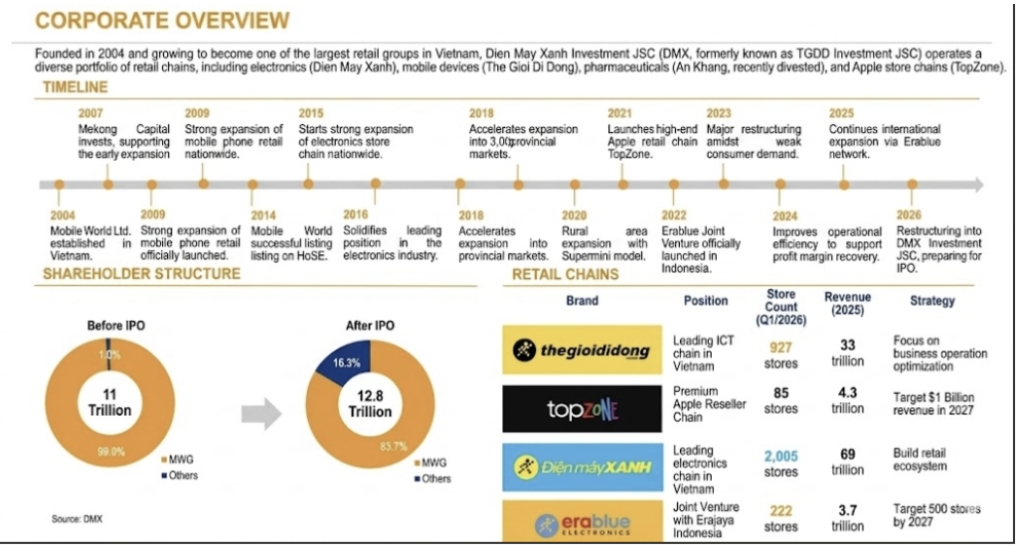

Over the past two decades, DMX's growth model was anchored in rapid network expansion - scaling store count to capture market share. The strategy proved highly effective, building a nationwide footprint of over 3,000 points of sale and driving market share from zero to a dominant 55%. With physical coverage now approaching optimal saturation, however, incremental store openings are no longer the primary growth lever.

CEO Doan Van Hieu Em offered the following analogy: "Think of it like growing a tree. The past two decades were about planting and nurturing it. Now we have entered the pruning phase - removing weaker branches and less productive parts so the core structure can grow stronger and support the next cycle of growth."

Reflecting a deliberate transition from volume-driven to quality-driven growth, DMX proactively closed approximately 400 sub-threshold stores between late 2024 and 2025. System-wide revenue not only remained resilient but recorded positive growth - validating the strategic rationale. This marks the first step of a five-year growth plan anchored in a five-pillar ecosystem: Operational Optimisation, Financial Solutions, Thợ Điện Máy Xanh, Super App, and international growth engine Erablue.

The CEO highlighted a defining shift in the Company's commercial philosophy: "Previously, delivery and installation of a television or refrigerator marked the conclusion of a transaction. Today, DMX goes beyond pure product sales - we deliver comprehensive solutions that enable customers to own and experience their products with maximum ease and completeness."

The strategy is executed through two complementary growth pillars: Flexible Financial Solutions and Lifecycle Services.

On Financial Solutions, DMX has addressed affordability barriers through instalment programmes of up to 24 months at optimised fee structures. The model is an effective demand stimulant in a recovering consumer spending environment, enabling customers to take immediate ownership of essential appliances without single-payment pressure - supporting both conversion and basket size.

On Lifetime Services, DMX is establishing a new benchmark in customer care. Taking air conditioners as an example, DMX offers an additional four-year extended warranty beyond the manufacturer's coverage, complemented by two complimentary maintenance services per year. This model unlocks a new recurring service revenue stream with margin-accretive characteristics, while also driving maximum brand engagement. When customers reach a replacement decision, DMX becomes the organic first choice - compounding retention and repurchase rates over time.

This deep customer engagement forms the strategic foundation underpinning DMX's next two growth pillars: the DMX Technician service network and the Super App platform.

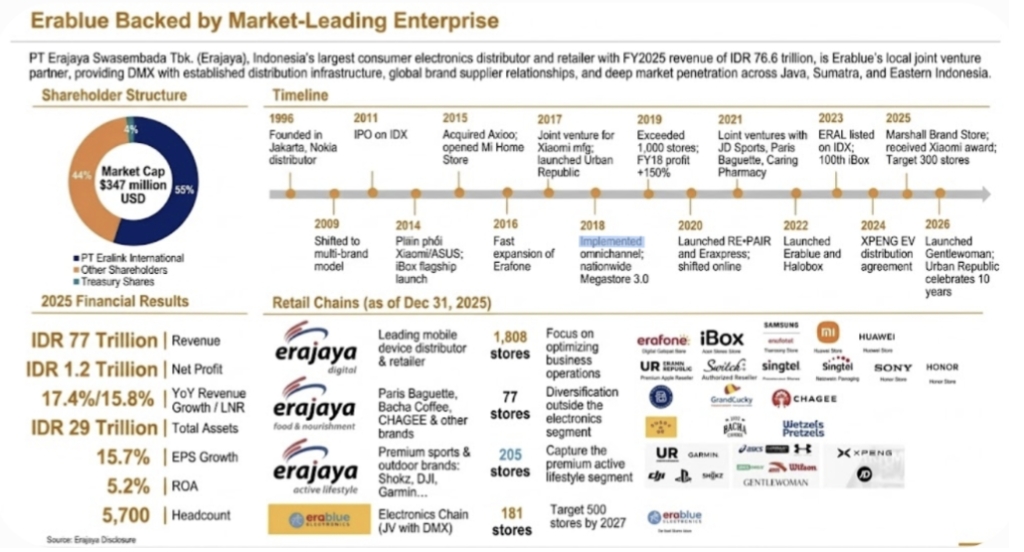

Indonesia: DMX's Next Growth Catalyst

While Vietnam represents DMX's home market at approximately 55% share, Indonesia is viewed as a greenfield opportunity. CEO Hieu Em noted that Indonesia's population is approximately 2.5 to 3 times that of Vietnam, with a higher GDP per capita - yet roughly 90% of the consumer electronics market remains fragmented across traditional trade channels.

Erablue is a joint venture between DMX and Indonesia’s Erajaya Group, where ownership is split 45%–55% in line with Indonesian foreign ownership regulations.

Three years into operations, with total invested capital of approximately USD 50 million, Erablue has grown to 250 stores and generated revenue of approximately VND 3,700 billion in FY2025.

Nonetheless, the current phase remains one of investment and model refinement ahead of full-scale acceleration. The Company targets 500 stores by early 2028, expanding to 1,000 stores by 2030 - with an associated revenue target of approximately USD 800 million.

Erablue's margins remain materially below those of the domestic Vietnam business. CEO Hieu Em noted, however, that this is broadly consistent with DMX's own development profile in its early years - more than a decade ago.

The CEO noted that as the network achieves sufficient scale, operational efficiency gains and enhanced supplier negotiating leverage should translate into margin improvement over time - consistent with the trajectory seen in the Vietnam business.

Average revenue per Erablue store is running at approximately 2.5 times that of comparable-format stores in Vietnam. For CEO Hieu Em, this validates the genuine depth of consumer demand in the Indonesian market.

Reframing the saturation thesis

Among the most persistent bear case assumptions surrounding DMX is that the consumer electronics retail market has reached saturation.

"At 55% market share, where does growth come from?" - a question DMX encounters consistently in the context of its IPO.

CEO Hieu Em responded directly: "One of the core objectives of this IPO is to reframe the market's saturation thesis on this sector."

The CEO noted that AI and emerging technologies are accelerating device replacement cycles. As laptops and smartphones accumulate compelling upgrade triggers after only a few years of use, sector-wide revenue can grow even without a material increase in unit volumes - a structurally positive dynamic for DMX.

The remaining approximately 45% of the market continues to be served by independent retailers and traditional trade channels. DMX views this as addressable share - to be captured not through price competition, but through superior service quality and the integrated offering that independent players cannot replicate.

"We have never wavered from that direction - to build a multi-category retailer spanning offline and online, domestic and international. That strategic direction was established more than a decade ago. We are now executing against it, systematically," said CEO Hieu Em.

CEO Hieu Em disclosed that upon completion of the listing, DMX intends to present a new incentive mechanism to the General Meeting of Shareholders for approval - one broadly analogous in structure to an employee stock option programme.

"If approved to proceed, we believe we would be among the first to pilot a mechanism of this kind. It will be distinctly different from a conventional ESOP," said CEO Hieu Em.

The CEO indicated the mechanism will be structured around multi-year targets spanning revenue growth, profitability, and market capitalisation - as distinct from a conventional ESOP. Performance criteria are set at a more demanding level, with the explicit objective of sustaining long-term alignment between the leadership team and shareholder value creation.

Source: VietnamBiz