Dien May Xanh: From Retail Expansion To Integrated Ecosystem, Targeting Net Profit VND 13 Trillion

In the 2022–2023 period, the market consensus was clear: the consumer electronics and mobile retail sector had reached saturation. Three years later, Dien May Xanh is entering its IPO journey with a bold target of VND 13 trillion in profit by 2030 - double the 2025 level - signaling a complete strategic pivot and the beginning of a new growth cycle.

A New Cycle: Profit Growth Outpacing Revenue

In its earlier phase, Dien May Xanh followed a classic retail expansion model: more stores meant higher revenue, which in turn drove profit. This model worked well in an underpenetrated market with limited competition. However, it also had a natural ceiling-once store expansion slows, growth inevitably plateaus. In 2022, MWG’s gross margin stood at 23.1%, while net margin was only 3.1%, reflecting the limitations of the model.

After restructuring, DMX - part of MWG and operator of thegioididong.com, Topzone, Dien May Xanh, EraBlue, and Tho DMX-has developed a new profit engine that does not rely on store expansion.

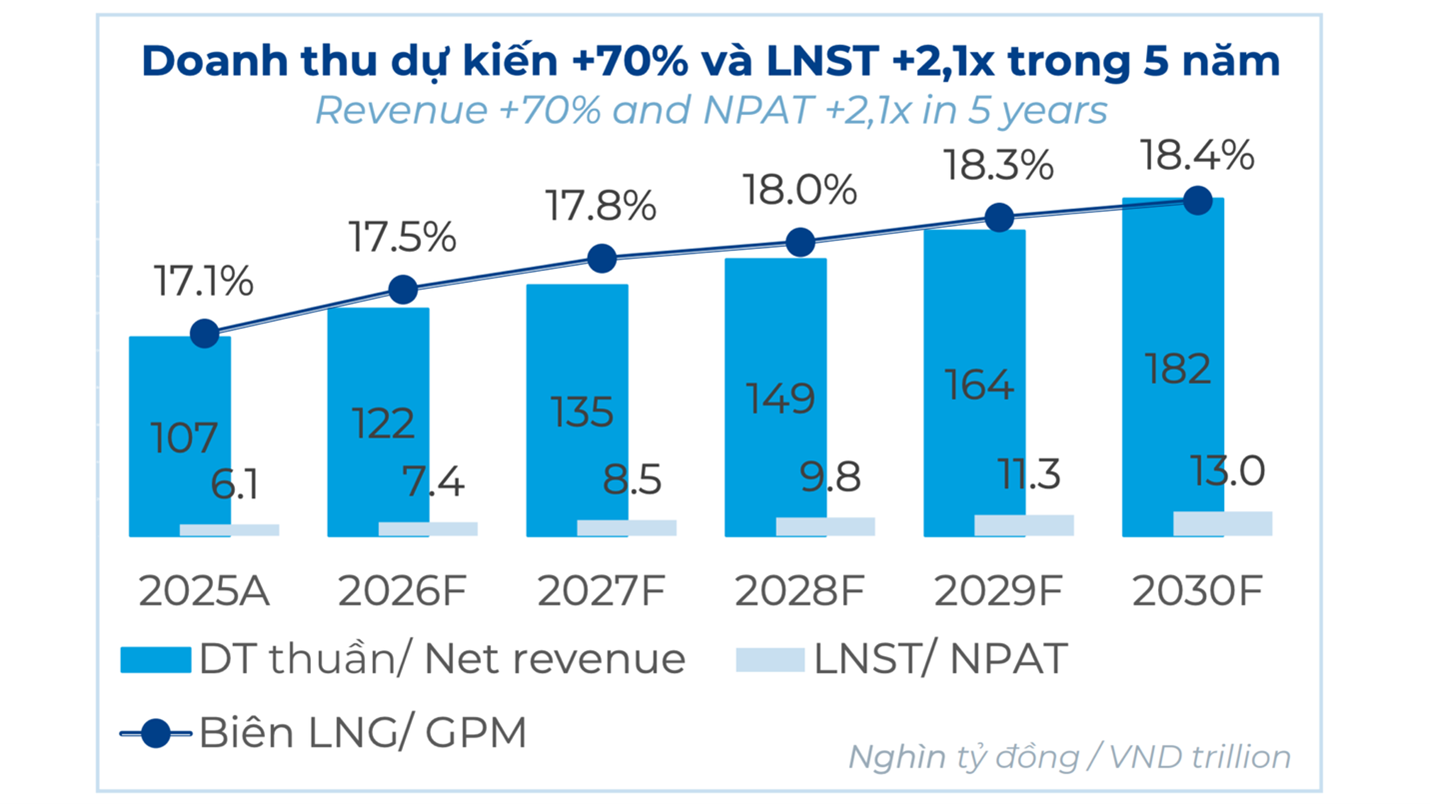

According to IPO materials, the company is shifting to a fundamentally different operating principle: prioritizing quality-driven growth over expansion. Without opening additional stores, revenue is projected to increase 1.6x to VND 182 trillion by 2030, while profit is expected to grow 2.1x to VND 13 trillion.

This implies a faster profit CAGR (16%) compared to revenue CAGR (11%), with gross margin expected to improve to 18.4% by 2030. The company also commits to a minimum 50% dividend payout ratio.

DMX “Money Machine” Model: Stable Revenue Growth, Stronger Profit Expansion. Photo: IR Website

At VAD 2026, CEO Doan Van Hieu Em emphasized that DMX is no longer positioning itself as a scale-driven retail chain, but as a high-margin, sustainable earnings platform built on every customer touchpoint. Once market coverage is achieved, physical expansion is no longer a priority.

This shift did not happen organically; it is driven by the fact that DMX possesses a unique bundle of competitive advantages that no single competitor in the region can match simultaneously: a physical retail network of 3,000 stores nationwide; 18 million verified customers - an asset that e-commerce platforms would have to spend hundreds of millions of dollars to acquire; and an integrated domestic logistics infrastructure consisting of 300 warehouses and 700 trucks.

Individually, each element may not appear extraordinary. However, when combined, they form a competitive moat that is difficult for either pure digital players or traditional retailers to replicate. This is precisely why the DMX IPO story is generating notable interest among investors.

5 Growth Engines Of Dien May Xanh’s “Money-Making Machine”

The IPO materials of Dien May Xanh outline five core growth pillars that transform the company from a pure retailer—selling products once—into a platform that captures the entire lifecycle of consumer technology usage. These five engines can be grouped into three that mainly improve operational efficiency, and two that have the potential to fundamentally re-rate valuation.

The first pillar focuses on optimizing pure retail operations. Dien May Xanh shifts from expanding store count to drive revenue toward optimizing each individual store to enhance profitability. Instead of viewing sales as the endpoint of a transaction, sales are now seen as the beginning of the customer lifecycle. This forms the foundation of the entire business architecture.

DMX applies ERP/CRM systems for inventory management, restructures its workforce based on performance, uses Topzone as a strategic bridge with Apple, and builds a “Familyship” culture with suppliers—treating partners as family. These initiatives help reduce costs and improve gross margin from 17.1% in 2025 to 18.4% by 2030.

The third pillar, “Tho DMX,” is expected to directly address key structural gaps in Vietnam’s home services market, including lack of price transparency, inconsistent technician quality, and the absence of a responsible party when issues arise.

The “Tho DMX” workforce consists of more than 8,000 fully standardized technicians, coordinated through ERP/CRM systems and supported by 300 warehouses and 700 trucks. This network serves not only 18 million internal customers but also expands to external retail customers, brands, and B2B partners.

The external service segment is projected to achieve a revenue CAGR of 65% and profit CAGR of 55%, driving total profits from the Thợ DMX business from VND 286 billion to VND 2,576 billion by 2030, accounting for 5.2% of total system profit.

A skilled technician team and dedicated logistics fleet enable DMX to fully control its end-to-end service chain, from installation to maintenance. Photo: DMX

The fifth pillar, EraBlue, serves as real-world proof that the DMX model can scale beyond Vietnam. In just three years since launch, EraBlue has become the No.1 consumer electronics chain in Indonesia with 181 stores and has achieved full-year profitability. Despite an average selling price only 70% of Vietnam’s level, revenue per store is 1.5 - 2.6 times higher than comparable DMX stores in Vietnam, and 50% of stores break even in the first month of operation.

Indonesia has a population three times larger than Vietnam and a mobile phone market 1.5 times bigger, yet its after-sales service infrastructure remains largely underdeveloped-precisely the gap the DMX model is designed to fill. The target is to scale from 181 to 1,000 stores, increase revenue from VND 3.7 trillion to VND 20.9 trillion, and grow net profit from VND 54 billion to VND 760 billion (70% CAGR), contributing around 3% of profit to the parent DMX system.

The remaining two pillars - consumer finance services and the Super App - are seen as potential game changers that could significantly reshape the valuation narrative if successfully executed.

The DMX consumer finance ecosystem provides financial solutions that make it easier for customers to access and own products, effectively sustaining and even stimulating demand.

DMX acts as an intermediary, connecting customers with consumer finance companies and banking partners directly at the point of sale, with an approval rate of over 80% and processing time of just 1–3 minutes. Four product layers are deployed simultaneously: installment payments via finance companies, BNPL (Buy Now Pay Later) wallets, credit card installment plans linked to 40+ banks, and personal consumer loans.

The structural shift is clear: the share of deferred payments is expected to increase from 35% in 2025 to 55% in 2030, while upfront payments decline from 65% to 45%. This model allows customers to pay with little upfront cost and longer repayment terms, without additional fees, thereby encouraging higher basket sizes.

In parallel, around 3,000 DMX stores are being transformed into payment and utility service hubs, enabling cash-in/cash-out services for 40+ banks and bill payments for electricity, water, and telecom services. The goal is to generate massive recurring traffic and transaction flows, with total transaction value projected to rise from VND 120 trillion to VND 275 trillion by 2030, and annual transactions increasing from 64 million to 150 million.

DMX does not primarily earn from interest income, but from service fees and commissions on this large transaction flow. This segment is expected to contribute around 15% of total gross profit by 2030.

The Super App serves as the integration layer of the entire ecosystem. According to IPO documents, it is not a traditional e-commerce platform and is differentiated by three key points: no need to purchase traffic thanks to 18 million verified customers; no price competition as it focuses on services and trust; and not purely digital, as it is tightly integrated with 3,000 physical stores and the Thợ DMX technician network.

Financial services - including installment payments, BNPL, and bill payments - are directly embedded into the platform, turning the Super App into a daily touchpoint rather than a transactional one.

Revenue through the Super App is projected to grow from VND 9 trillion to VND 55 trillion (44% CAGR), accounting for 30% of total system revenue by 2030.

Valuation Question: Which Industry’s P/E Multiple Applies?

Vietnam’s consumer electronics market is projected to reach USD 15 billion by 2030, with a compound annual growth rate (CAGR) of 8.2%. This means the total market is not stagnant - it is expanding in line with technology upgrade cycles, the AI-5G-smart home wave, and a growing middle class.

In 2025, while the overall market grew by 13%, DMX grew by 18%, despite not opening any new stores - effectively gaining market share in a mature format.

The “saturation” narrative often applied to this sector may need to be reconsidered from two perspectives: the overall market scale and growth trajectory, and the performance of the market leader, Điện Máy Xanh.

With DMX’s IPO plan, investors may need to reassess whether it is appropriate to apply traditional retail valuation frameworks to a business that is transitioning into a platform model.

Best Buy, the largest electronics retailer in the U.S., was once widely labeled as a declining business, yet it is now valued significantly higher than several European electronics chains that have effectively disappeared. The key reason: its successful transition into a services-driven model via Geek Squad and Total Tech Support - a direction similar to DMX’s Thợ Điện Máy Xanh strategy.

JD.com in China presents another case: its O2O platform integrating logistics and in-store financial services is valued using platform-level P/E multiples rather than traditional retail multiples.

This shows that DMX is not inventing a completely new model, but localizing a globally validated trend, while leveraging a physical infrastructure advantage that pure digital competitors cannot replicate.

However, alongside the upside, risks also exist. For investors, the key risk is not strategy, but execution capability across these growth pillars.

For example, the Super App requires large-scale behavioral change among users - a challenge that even well-funded Southeast Asian platforms have taken years to overcome. Meanwhile, consumer finance depends heavily on the risk appetite of financial partners, which is outside DMX’s direct control.

Similarly, scaling Erablue from 181 to 1,000 stores represents a fundamentally different operational challenge.

These risks do not invalidate the story; they simply mean it must be evaluated through execution rather than IPO narratives. DMX itself states that the IPO is intended to reflect fair valuation, enable independent operations, and improve transparency, while addressing the long-standing “saturation” perception of the electronics retail sector.

Ultimately, DMX needs to convince the market that every customer interaction - whether in one of its 3,000 stores or on its Super App - is the beginning of a long-term sequence of financial transactions, service engagements, and digital touchpoints spanning multiple years.

Source: Vietstock